Exhibit 12b- Breakdown of 'other' complaints received in 2023/24 into key themes

Toggle pie chart

This year has been marked by a strong focus on continuous improvement, building on the momentum established in the previous year. The first year of our Strategic Plan has provided a clear and consistent framework to guide our priorities and actions throughout 2024/25. The table below outlines the progress made against the strategic objectives.

| Strategic Objective | Progress made in 2024/25 | ||

|---|---|---|---|

Standards | Public Appointments | Corporate | |

| 1. Stakeholder and public engagement | ✔ Strong engagement across key networks – Society of Local Authority Lawyers and Administrators (SOLAR) and Convention of Scottish Local Authorities (COSLA) etc ✔ Active role in stakeholder workshops with Monitoring Officers and Standards Officers ✔ Produced Easy Read guides for the public to simplify our process ✔On-going collaboration with Standards Commission for Scotland (SCS) ✔ Stakeholder analysis using Boston Matrix ✔ Website improved for easier access | ✔ Direct contact during workshops with public body chairs and members as part of our research into time commitment and remuneration ✔ Conducted applicant surveys at the conclusion of appointment rounds ✔ Held four communication events for Public Appointments Advisers (PAAs) ✔ Ongoing collaboration with the Scottish Government Public Appointments Team ✔ Direct contact with panel chairs and body chairs through seeking views on PAA performance, research projects and answering queries | ✔ Ensured each team understood ESC’s five key messages for stakeholders ✔ Launched the cross-functional Accessibility Working Group to identify and develop alternative formats for communicating with stakeholders |

| 2. Sufficient resources, resilient and valued staff and shared services. | ✔ Staff reviews conducted in accordance with performance framework ✔ Individual tailored training plans in place for all staff ✔ Good practice shared with equivalent regulators in other UK administrations | ✔ Staff reviews conducted in accordance with performance framework ✔ Individual tailored training plans in place for all staff ✔ Supportive guidance to officials in Scottish Government and public bodies | ✔ Renewed the organisation’s Scheme of Delegation ✔ Full cross-functional engagement when preparing the budget submission ✔ Active membership of the Officeholders Shared Services Network ✔ Completion of annual staff wellbeing survey ✔ Introduction of quarterly, in person staff training and communication days |

| 3. Staff training, support and development | ✔ Over 50 hours of targeted training delivered ✔ Appraisals completed on time and to high standards ✔ Tailored personal development plans in place ✔ Zero staff turnover maintained ✔ Regular manager check-ins and focussed mentoring support ✔ Team and case review meetings held to share best practice and continuous learning | ✔ Appraisals completed on time and to high standards ✔ Tailored personal development plans in place ✔ Zero staff turnover maintained | ✔ 22 training events arranged or co-ordinated for individuals, each team or the whole organisation ✔ Annual all staff training on Data protection, Freedom of Information and Cyber security completed ✔ Arranged ESC access to Civil Service Learning Platform ✔ Appraisals completed on time and to high standards ✔ Tailored personal development plans in place ✔ Zero staff turnover maintained |

| 4. Up to date and secure digital technology and records management | ✔ All records reviewed and updated per the records management plan ahead of Sharepoint migration ✔ Improvements to the Complaints Management System to improve performance monitoring and case tracking | ✔ All records reviewed and updated in accordance with records management plan prior to Sharepoint migration | ✔ Migration to SharePoint ✔ Cyber Essentials Plus re-accreditation ✔ Introduced 2 Factor Authentication to all ESC-run web services ✔ Brought majority of records in line with retention schedule ✔ Completed 30 information requests |

| 5. Efficient and effective complaints handling | ✔ Stage 1 average waiting times halved since early 2024/25 ✔ Stage 2 average waiting time decreased by 17% v 2023/24 ✔ 36% increase in cases completed v 2023/24 ✔ Duty Investigating Officer (DIO) triage introduced to streamline intake ✔ Improved case allocation and workload balance ✔ Investigations Manual regularly reviewed and updated ✔ New templates introduced for clarity and speed ✔ Improved use of Case Management System (CMS) to enhance waiting times management | ||

| 6. Governance, quality review and external accreditation | ✔ Peer Review process embedded ✔ Quality assurance (QA) framework implemented ✔ Continuous improvement drive by QA ✔ Revised Key Performance Indicators (KPIs) established for performance tracking ✔ Scheme of Delegation in place, working well and regularly reviewed | ✔ Organisational risks reviewed on a quarterly basis – during the year four new risks were identified, four fell away and seven risks carried forward ✔ 42 policies and procedures reviewed with two outstanding at year end | |

| 7. Ethical Standards Network (ESN) maintenance | ✔ Ethical Standards Network re-established with regular meetings ✔ Shared training, resources, and good practice in place ✔ On-going meetings and engagement with other UK Commissioners ✔ Developed training and guidance with SCS, for councillors and members | ||

| 8. Supportive and constructive regulation of public appointments | ✔ Published Strategic Plan in EasyRead ✔ Applicant surveys run following appointment rounds (when information provided to us by the Scottish Government (SG)) ✔ Views sought from panel chairs and body chairs on performance of PAAs ✔ Project plan underway to review website based on feedback ✔ Training (Briefing) provided to panel members on request (e.g. on Parliamentary scrutiny) and to SG Public Appointment Team (SG PAT) members as part of induction ✔ Training and support of NHS work such as “aspiring chairs of the future” ✔ Ongoing support for panels and PAAs on aspects of the Code and guidance ✔ Successful internal audit of database system used to ensure consistent decision-making | ||

| 9. Recognised leaders in the regulation of public appointments | ✔ Collation of information at the end of each appointment round to try and identify themes ✔ Ongoing collaboration with SG PAT ✔ Good practice case studies developed and published ✔ Good practice “snippets” developed and published ✔ Interim report on applicant views written and published ✔ Commencement of thematic review (due to be published in later 2025) ✔ Commencement of the review of the Diversity Strategy ✔ Annual Service Level Agreement review carried out with each PAA ✔ Training provided for PAAs on four occasions through the year ✔ Regular communication briefings (including guidance / training) throughout the year. | ||

You can find out more about our progress towards achieving our strategic objectives on the Metrics page that will be published on our website.

Our strategic objectives during 2024/25 are drawn from the from the Revised Strategic Plan 2024 to 2028:

1. | We will engage meaningfully with our stakeholders and the public to promote high standards in public life and adherence to the principles of public life in Scotland. We will take on board feedback, listen to others’ views and work constructively to improve our systems and processes. |

2. | We will ensure that we have sufficient staff and resources in place to deliver on all of our objectives, building resilience and flexibility across roles and remits. We will also work with other Parliamentary Officeholders with a view to embracing efficiency and innovation through shared services. We value people and recognise that unless we have staff who are valued and supported to maintain their wellbeing, feel happy in and proud of our work and the way in which we do it, we will have failed. |

3. | We will ensure that our staff are properly trained, supported and developed to fulfil the requirements of their role and their career progression. |

4. | We will make the best use of up to date and secure digital technology to support our work, enhance our users’ experience and safeguard our systems. |

5. | We will operate highly efficient and effective complaints handling processes that deliver consistent, evidence-based responses: ensuring fair and trusted outcomes. |

6. | We will ensure appropriate systems of governance, quality review frameworks and robust external accreditation are in place, providing assurance to the public and stakeholders that our objectives are being met. We will also demonstrate our commitment to acquitting our environmental and social responsibilities. |

7. | We will contribute significantly to the maintenance of an effective ethical standards framework through supportive and constructive engagement with equivalent bodies both here and in other administrations. |

8. | We will, through supportive and constructive regulation, make a significant contribution to a public appointments system that produces effective and diverse boards that are reflective of the communities that they serve. |

9. | We will strive to be recognised leaders in the regulation of a system that is effectively run to achieve the appointment of the most able people to our boards and that is managed in compliance with the highest ethical standards. |

Our strategic plans are supported by biennial business plans. These detail the actions we will take over a rolling two-year period to achieve our strategic objectives. Progress against these objectives as at 31 March 2025 is set out in the Biennial Business Plan for 2024-2026 available on our website.

The Biennial Business Plan for 2025-2027 is also available on our website.

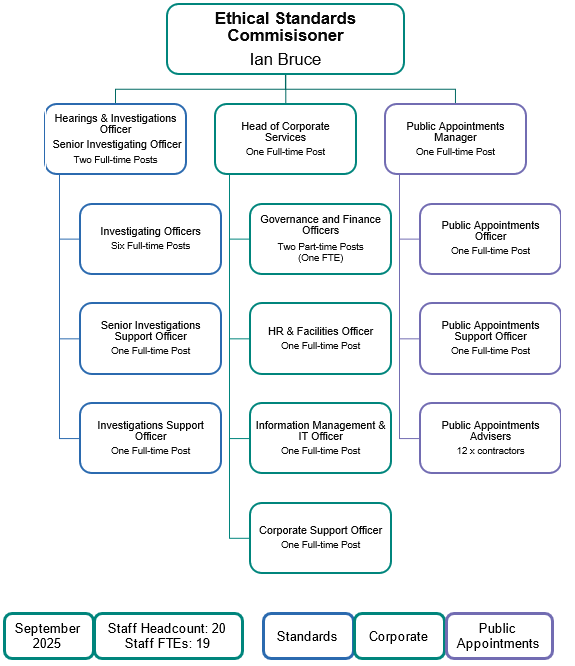

Led by Senior Investigating Officer and Hearings and Investigating Officer*:

Led by Head of Corporate Services:

Led by Public Appointments Manager:

*The Senior Investigating Officer (SIO) and Hearings and Investigations Officer (HIO) jointly manage and oversee the work of the Standards Team. Line management for the team is split equally between the SIO and HIO.

The Commissioner’s primary functions are:

This report provides an update on the progress that we have made against our strategic objectives in the first year of our 2024-28 strategic plan. The plan itself is very clear about the values that we hold dear as an organisation and which inform all of our activities.

Our objectives cover a range of activities intended ultimately to improve public confidence in the ethical standards framework and the regulated public appointments system in Scotland. They include:

I am content that we have made great strides in all of these areas during the course of the year, with progress driven by a highly focussed and effective team. I highlight our key achievements in this opening statement, but the list is not exhaustive. More detail is provided in the body of this report and on our website, reflecting our commitment to transparency.

We did experience some challenges relating to turnover in the Scottish Government’s public appointments team (PAT). We sought to support them during this challenging period, as when they are stable, they can add significant value. Part of the problem attached to this turnover is the clear loss of corporate memory and the impact this has on the adoption and roll out of good practice. The Scottish Government should have a system in place to address this so we will continue to make our expectations in this area clear.

As with all public sector organisations, we faced risks during the year relating to issues such as pressures on the public finances, IT failures and staffing. We have robust processes and plans in place to mitigate these, as can be seen from the range of successfully completed actions set out above.

The extent of our success in achieving the challenging programme of activities in the year is entirely attributable to the dedicated team of professionals working at every level within the organisation. They are diligent, bright and motivated to do their best for the many stakeholders whose expectations of us are rightly very high.

I endeavour to meet these same standards but also to be the public face of the organisation in what can be challenging circumstances. Incivility in public life continues to increase and it is incumbent on me to call it out and to highlight the negative impact of it on democracy. This will be a priority for me in the year ahead.

Ian Bruce

Ethical Standards Commissioner

03 October 2025

This section of the report provides a summary of our performance as well as outlining any significant activities undertaken during the year. It also describes the organisation’s purpose and the key risks affecting it.

For the Commissioner for Ethical Standards in Public Life in Scotland known as the Ethical Standards Commissioner (ESC).

This report is available in PDF and alternative formats on request by telephoning 0131 347 3890 or by e-mailing info@ethicalstandards.org.uk.